When you think about money, and how it moves around, there is a very important idea that often comes up. This idea, called Annual Percentage Rate, or Apr-60 as we are calling it here, is something that touches your financial life in quite a few ways. It is, you know, a key piece of information for anyone who borrows money or even puts money away to earn something back. Basically, it helps you see the real cost or benefit involved.

So, this Apr-60, it is more than just a bunch of numbers on a paper. It represents the yearly amount of interest that money makes, whether it is being charged to someone who has taken out a loan or it is being paid to someone who has put their money into an investment. It is, in a way, a simple percentage that helps to show the full picture of what you are paying or what you are getting.

This discussion will help you get a better grip on what Apr-60 means for things like credit cards and various kinds of loans. We will look at the different sorts of Apr-60 that exist, what kinds of things can change your interest rate, and, well, how you might go about getting a rate that works better for you. It is really about giving you a clearer picture of your financial dealings.

- Johanna Flores

- Diddy Michael Jackson House Tunnel

- Garcelle Net Worth 2024

- Lee And Tiffany Divorce 2020

- Dominik Mysterio And Rhea Ripley Together

Table of Contents

- What is Apr-60, Really?

- What Makes Up Your Apr-60?

- What Affects Your Apr-60?

- Why is Apr-60 a Big Deal for Your Decisions?

- Apr-60 - More Than Just Money?

What is Apr-60, Really?

Apr-60, which stands for Annual Percentage Rate, is a pretty important idea in the financial world, you know. It talks about the yearly interest that money generates. This interest can be something that is charged to people who are borrowing funds, or it could be something that is paid out to people who are putting their money into an investment. It is, basically, a way to show the yearly cost or return of money, expressed as a percentage number.

When someone asks, "what is Apr-60 on a loan?", they are really asking about this yearly cost. It is a way to look at how much you are truly paying to use someone else's money for a set period. Similarly, for those who are investing, it shows how much their money might grow over a year. So, it is a rather straightforward way to grasp the financial implications of a sum of money over a twelve-month period.

This Apr-60 figure is a measure that helps you see the total yearly expense of using money. It is, in some respects, a more complete picture than just looking at the simple interest rate. It takes into account not just the interest, but also other charges that might come along with borrowing money. This means it gives you a much better idea of the actual expense you are taking on.

It is almost like a common language for comparing different financial offerings. When you see Apr-60 expressed as a percentage, you get a quick way to size up various loans or credit card offers. This percentage represents the overall yearly burden or gain, helping you to make sense of what might otherwise seem like a lot of confusing numbers and terms. It is, really, a key piece of information for making sensible choices.

How Does Apr-60 Show Up in Your Life?

You have probably come across the term Apr-60 quite a bit, maybe without even thinking much about it. It is that phrase you often see in various financial papers or hear when people are talking about things like loans and credit cards. It is, you know, a very important idea that is always there when you are dealing with borrowed money or even when you are considering putting your money into something that might grow.

When you are looking at credit products, for example, like credit cards, or perhaps a loan for a car, or even a home loan, Apr-60 is a term that gets used a lot. It is, basically, the rate that helps to determine the cost of using that credit. This rate, in short, helps to set the amount you will pay over time for the privilege of borrowing. It is pretty much always there in these kinds of discussions.

For credit cards, if you do not pay off your entire balance each month, the card issuer will charge you interest on the amount you still owe. This interest is calculated using the Apr-60 that is tied to your card. So, it is, like, a direct way that Apr-60 affects your wallet if you carry a balance. It is a very real part of how credit card accounts work for many people.

In the case of loans, whether it is for a house or a car, the Apr-60 helps you to understand the total yearly cost of that loan. It is not just the simple interest rate, but also other fees that might be involved. So, it is, in a way, a more complete picture of the expense. This means that Apr-60 is a concept that is pretty much always present when you are thinking about borrowing money for any significant purchase.

What Makes Up Your Apr-60?

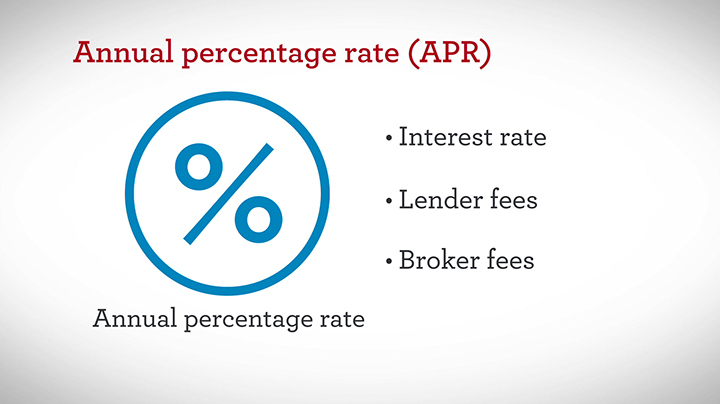

The Apr-60 is, actually, a measure that takes into account all the usual costs of borrowing money. It is more than just the basic interest rate you might see. It includes things like discount points, which are a kind of fee paid to reduce the interest rate, and also closing costs, which are expenses tied to getting a loan, especially for a house. All these different costs are then shown as one simple percentage, which is the Apr-60. It is, basically, a way to package up all the financial bits into one easy-to-understand number.

It is important to remember, though, that the Apr-60 does not include absolutely every single possible fee or charge. There might be some very specific fees that are not rolled into this percentage. However, it does capture the main, standard costs that you would typically expect when you borrow money. So, it is, you know, a very helpful tool for getting a general idea of the total expense of a loan, even if it is not absolutely exhaustive.

The core of Apr-60 is, of course, the interest rate itself. This is the basic cost of borrowing the money. But then, other elements are added to this. For example, if you are getting a mortgage, there might be origination fees, processing fees, or even charges for things like appraisals. These are all folded into the Apr-60 calculation to give you that single, yearly percentage figure. It is, in some respects, a bit like a financial summary of all the key charges.

So, when you see an Apr-60, you can think of it as the yearly cost of a loan, expressed as a percentage. This percentage, basically, includes your interest rate and any extra fees you will be charged for taking out the loan. As a result, Apr-60 is a much more complete way to measure how much a loan truly costs you each year. It is, really, a comprehensive way to look at the financial burden.

Are There Different Kinds of Apr-60?

Yes, there can be different sorts of Apr-60, which is something important to know. The Apr-60 you get can be either fixed or variable. This difference can, you know, have a pretty big impact on how much you end up paying over the life of a loan. It is, basically, about whether the rate stays the same or if it can change over time.

A fixed Apr-60 means that the rate of interest and fees that you are charged will stay the same for the entire period of the loan. This means your monthly payments for that part of the loan will be predictable, which can be very helpful for planning your budget. It is, in a way, a stable choice, offering a clear path forward with your payments.

On the other hand, a variable Apr-60 means that the rate can change. It is usually tied to a market index, so if that index goes up or down, your Apr-60 can also go up or down. This means your payments could change over time, which might be a bit less predictable. So, it is, like, a rate that moves with the market, offering a different kind of financial experience.

Knowing whether your Apr-60 is fixed or variable is, actually, a very important part of making an informed choice about borrowing money. It helps you to understand the potential for your costs to change, or to know that they will remain steady. This understanding is, really, a key piece of information for anyone considering a loan, as it affects the long-term financial picture.

What Affects Your Apr-60?

There are, actually, several things that can influence the Apr-60 you are offered for a loan or credit card. These factors often relate to how risky a borrower someone might seem to a lender. For example, your credit history, which is a record of how you have managed borrowed money in the past, plays a pretty big part. A history of making payments on time and managing credit well can lead to a more favorable Apr-60. It is, in some respects, about showing you are a reliable person when it comes to money.

The type of loan you are getting can also affect the Apr-60. For instance, a home loan might have a different range of Apr-60s compared to a personal loan or a car loan, because the risk associated with each type of borrowing is different. So, the very nature of what you are borrowing for can influence the rate you are offered. It is, basically, about the specific financial product you are choosing.

Market conditions also play a role, you know. The general state of the economy and interest rates set by central banks can influence what lenders are willing to offer. If overall interest rates in the market are low, you might find that Apr-60s are also generally lower. Conversely, if rates are high, then the Apr-60s you see might also be higher. It is, really, a reflection of the wider financial environment.

The loan amount and the length of time you plan to pay it back can also have an impact. Sometimes, a larger loan amount or a shorter repayment period might come with a slightly different Apr-60. It is, like, a combination of all these elements that lenders consider when they decide what Apr-60 to offer you. So, it is not just one thing, but a mix of various financial details.

Getting a Better Apr-60 - Is That Possible?

Yes, getting a lower Apr-60 is often possible, and it is something many people aim for because it means paying less over time. One of the main ways to work towards a better Apr-60 is to have a good financial standing. This often means having a solid record of paying bills on time and keeping your credit use sensible. Lenders, you know, tend to see people with good financial habits as less risky, which can lead to better rates.

It is also a good idea to compare offers from different lenders. Different banks or credit providers might have different ways of assessing risk and different pricing structures. So, what one lender offers for an Apr-60 might be different from another. By looking around and comparing, you can, basically, find the offer that is most favorable for your situation. It is, in a way, like shopping around for the best deal.

Sometimes, having a co-signer on a loan, someone who agrees to pay if you cannot, can also help you get a lower Apr-60, especially if your own financial history is not as strong. This is because the co-signer adds another layer of security for the lender. So, it is, like, another option to consider if you are looking to reduce the cost of borrowing.

Understanding what factors influence your interest rate and then taking steps to improve those factors can help you secure a better Apr-60. This can lead to making more informed borrowing decisions and, ultimately, saving you money over the life of a loan. It is, really, about being proactive with your financial choices.

Why is Apr-60 a Big Deal for Your Decisions?

Understanding Apr-60 is, actually, very important for making good decisions when you are borrowing money. It is the yearly cost of a loan, expressed as a percentage, and it includes your interest rate plus any extra fees you will be charged. So, it is, basically, a more complete way to measure the true cost of using borrowed funds. This means you can see the full financial picture before you commit to anything.

When you are comparing different loan offers, looking at the Apr-60 allows you to compare them on an equal footing. A loan might have a low interest rate, but if it has a lot of fees, its Apr-60 could still be high. Conversely, a loan with a slightly higher interest rate but fewer fees might have a lower Apr-60. So, it is, like, the best way to truly compare the total expense of one loan versus another.

Apr-60 affects how much money you will pay back over the entire period of the loan. A higher Apr-60 means you will pay more in total, while a lower one means you will pay less. This has a direct impact on your budget and your long-term financial health. It is, in a way, a very clear indicator of the financial burden you are taking on.

By truly understanding Apr-60, you can make choices that are better for your wallet. It helps you to avoid surprises and ensures you are aware of the full financial commitment involved. This knowledge is, really, a powerful tool for anyone dealing with credit or loans, helping you to plan your finances with greater confidence and foresight.

Apr-60 - More Than Just Money?

While most of our discussion about Apr-60 has been about its financial meaning, there is, actually, another use of the term "APR" that is quite different. It is, apparently, also the name of a company that started back in 1997. This company, APR, is a global leader in products for improving the performance of certain vehicles.

This other APR develops and makes hardware and software for cars like Volkswagen, Audi, Seat, Skoda, Porsche, and other vehicles. So, it is, you know, a completely different context for the letters "APR." It is a company focused on making cars run better, rather than a financial rate.

It is interesting how the same set of letters can mean such different things depending on the conversation. In this case, one "APR" is about the cost of money, and the other "APR" is about making car engines more powerful. So, it is, like, a good reminder that context matters a lot when you hear certain terms.

This discussion has covered what Annual Percentage Rate, or Apr-60, means in the financial world. We have looked at how it represents the yearly cost of borrowing or the return on investing, expressed as a percentage. We explored how it helps compare different financial products like credit cards and loans, and what components make up this rate, including interest and various fees. We also touched upon the difference between fixed and variable Apr-60s, and what factors can influence the rate you receive. Furthermore, we discussed why understanding Apr-60 is so important for making smart financial decisions. Finally, we briefly noted that "APR" can also refer to a company involved in automotive performance products, highlighting the importance of context.

- Trisha Paytas Naked

- My Pillow Pillow Topper

- Does Lorelai And Max Get Married

- Number Time Babyfirst Tv

- Julia Gilbert